Our offices frequently get calls regarding student loan debt, and we have to give those callers the same disappointing answer: “Student loans are not typically dischargeable under either chapter 7 or chapter 13 bankruptcy. While those forms of bankruptcy may eliminate or reorganize the majority of your debt so that you are able to repay your student loans, they are not currently structured to allow a complete discharge of student loan debt.”

To be honest with you, we wish we had a different answer because it would be great for business; however, as the current bankruptcy rules stand, there are extremely few circumstances under which a person can be discharged from their student loan debt within the bankruptcy process. I’m not being pessimistic when I say extremely few; I might actually be understating the level of difficulty. However, if you are going to attempt to get rid of your student loan debt through bankruptcy then you’ll want to learn about the phrase “Undue Hardship Exception” and The Brunner Test.

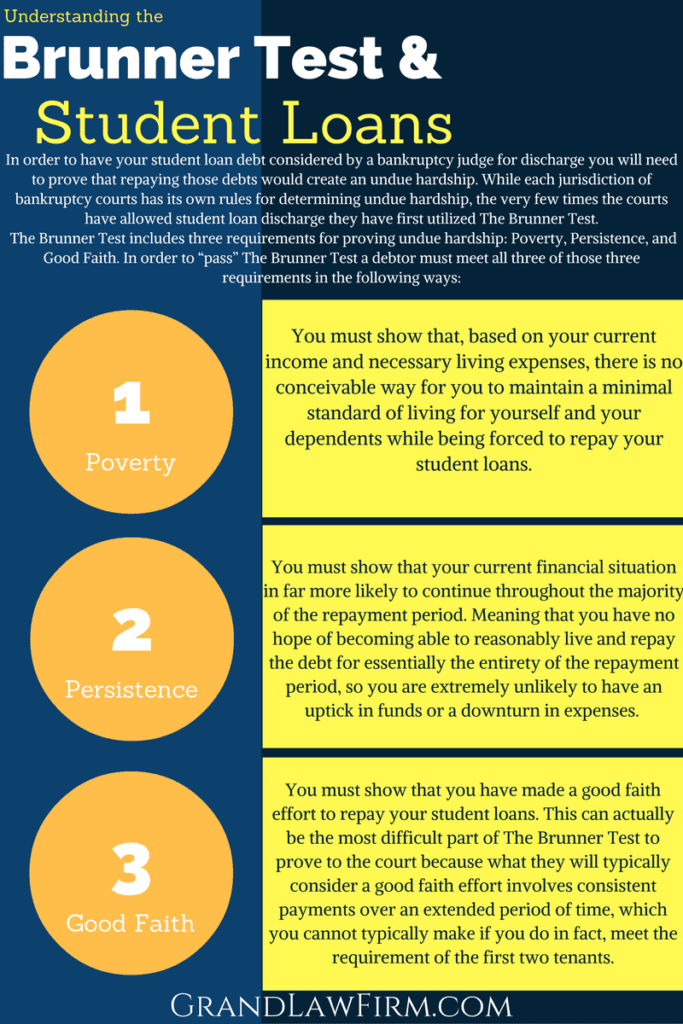

In order to have your student loan debt even considered by a bankruptcy judge for discharge, you will need to prove that repaying those debts would create an undue hardship. While each jurisdiction of bankruptcy courts has its own rules for determining undue hardship, the very few times the courts have allowed student loan discharge they have first utilized The Brunner Test.

The Brunner Test includes three requirements for proving undue hardship: Poverty, Persistence, and Good Faith. In order to “pass” The Brunner Test a debtor must meet all three of those three requirements in the following ways:

Poverty: Based on your current income and necessary living expenses, there is no conceivable way for you to maintain a minimal standard of living for yourself and your dependents while being forced to repay your student loans.

This requirement of The Brunner Test is somewhat similar to the means test that one must “pass” before filing for chapter 7 bankruptcy, but with more strenuous requirements for proving a minimal standard and justification for expenses.

Persistence: You must show that your current financial situation is far more likely to continue throughout the majority of the repayment period. Meaning that you have no hope of becoming able to reasonably live and repay the debt for essentially the entirety of the repayment period, so you are extremely unlikely to have an uptick in funds or a downturn in expenses.

Good Faith: You must show that you have made a good faith effort to repay your student loans. This can actually be the most difficult part of The Brunner Test to prove to the court because what they will typically consider a good faith effort involves consistent payments over an extended period of time, which you cannot typically make if you do, in fact, meet the requirement of the first two tenets.

While establishing that you meet all three of these tenets in such a way that documentation can be gathered and presented to the courts is the first step to seeking a discharge from your student loans through bankruptcy, it is important to remember that these requirements are extraordinarily difficult to prove to a bankruptcy judge. Ultimately, once you’ve gathered and prepared all of your information, you will need to file a formal complaint with the bankruptcy court, called a Complaint to Determine Dischargeability. After your complaint is filed, the bankruptcy judge will review your documentation and deliver a judgment. Once that judgment is passed down it is unlikely to change, which is why it is imperative you have all of your information complete and comprehensive on your first attempt.

For more information regarding bankruptcy and other debt relief options, please contact our Baton Rouge or New Orleans office for a free consultation.